International Issues to Watch in 2019

Theresa May & Donald Tusk

January 3, 2019

As 2018 comes to a close, one of its striking characteristics is the head-spinning pace of developments in domestic and international affairs. Another is the rising sense that political risks could blow the global economy off course. One year ago, growth was occurring everywhere, and business forecasts were the rosiest in years. While there were plenty of political risks in 2018—U.S.-China relations, Brexit, NAFTA, North Korea, Saudi Arabia, Iran, and pivotal elections in Italy, Mexico, Brazil, and the United States—market sentiment sailed past them. Now, however, global growth is moderating, markets across the board are falling, and the world feels tense.

This fast-moving and complex dynamic makes it difficult to form a view of the future. As such, this brief reviews developments over the last year and uses conceptual frameworks to suggest how the year ahead may unfold.

U.S.-China: “Cold War II”

Over the past 30 years, the West, and America in particular, has equated China with business opportunity. This attitude fueled China’s globalization and economic development, and in the process, China evolved from an emerging market into a superpower—one that dominates Asia and shapes global goods and capital flows, technology development, and, even, the climate. Lately, China has come to be seen not as an opportunity but as a threat. This shift in perception was the dominant geopolitical development in 2018, and it is going to shape the global business environment in 2019 and for many years, perhaps decades, to come.

At the start of 2018, U.S.-China tensions were framed as a trade dispute. U.S. tariffs were aimed at rebalancing trade in manufactures between the two countries, with opponents of the measures arguing that tariffs were bad for costs, supply chains, and consumers. Since then, the field of play has quickly expanded, and there is much more at stake. In remarks to the U.S. Senate in March, Admiral Philip Davidson, the commander of the U.S. Indo-Pacific Command, asserted that China’s navy was “capable of controlling the South China Sea in all scenarios short of war.”

Around the same time, then-Defense Secretary Jim Mattis signed off on a new National Defense Strategy that labeled China a “strategic competitor” that uses “predatory economics” and is “undermining the international order from within the system by exploiting its benefits while simultaneously undercutting its principles.” Treasury Secretary Steven Mnuchin has also been using his platform to warn countries against accepting Beijing’s Belt and Road infrastructure projects lest they get trapped in crushing debt spirals that lead to Chinese asset stripping.

Beijing had hoped that President Trump’s wings would be clipped with Democratic victories in the U.S. midterms. That hope was misplaced, as China has become a bipartisan threat.

The business media, too, has shifted from lamenting the risks to free trade by a misguided White House to breathless investigative reports about China’s cheating on trade, use of prison labor, cyberwarfare, and technology and data theft. In this worldview, costs and consumers have become secondary concerns.

The changing China narrative in 2018 is reminiscent of the situation in 1946, when the perception of the Soviet Union quickly shifted from one of an exhausted World War II ally to one of a menacing bear that was sponsoring antidemocratic insurgencies and drawing an Iron Curtain across Europe. Washington’s response to the Soviet “menace” was halting and haphazard at first, but it developed into a comprehensive strategy of military, economic, and ideological containment backed by a network of alliances.

The Trump administration’s approach to China has been to barrage Beijing on a number of fronts. Beijing had hoped that President Trump’s wings would be clipped with Democratic victories in the U.S. midterms. That hope was misplaced, as China has become a bipartisan threat. Both Democrats and Republicans have broadly concluded that the United States needs to adopt firm measures to rebalance economic, geopolitical, and technological relations. And while the White House has been stymied on many policy fronts and threatened by investigations, it has found that being tough on China is a winning political formula.

Despite the political science school of thought that argues that trading nations do not go to war, international businesses and investors are getting caught in crossfire between China and the United States.

As the United States gears up for the 2020 presidential election, Democrats are going to be tripping over themselves to show that they can be even tougher. Finally, the EU and Japan, despite their frustrations with the White House, are quietly aligning with Washington to confront Beijing on trade, investment, and technology policy. Even as U.S. markets stumble, the White House still feels it has momentum. As with North Korea, claims of rapprochements will likely be rhetorical.

On the other side of the equation, President Xi Jinping has consolidated his hold on the leadership and is using nationalism to boost support for the Communist Party. His signature goal is to make China great again and he said that his country won’t succumb to American “bullying.” Discussions to defuse the conflict have been episodic. In December, following a dinner meeting of the two presidents, Beijing offered to dial back tariffs on American autos and indicated that it was prepared to resume agricultural purchases from the United States.

Reports also emerged that the government was going to rework the Made in China 2025 strategy, which aims for supremacy in critical technologies. Beijing has also been adjusting the formula of its Belt and Road Initiative. But these recalibrations are likely to be largely cosmetic and certainly will not meet the aggressive economic containment objectives the White House has laid out. Beijing has also made clear that it will not be deterred from pursuing its long-term economic and geostrategic ambitions.

During the Cold War, U.S. trade with the Soviet Union was minimal: in a landmark deal, Stolichnaya was bartered for Pepsi-Cola. But the United States and China have the world’s deepest trade and investment relationship, and despite the political science school of thought that argues that trading nations do not go to war, international businesses and investors are getting caught in crossfire between the two countries.

In short, China-U.S. relations are likely to get worse before they get better.

Business leaders on both sides of the Pacific will have to adjust to the new geopolitical context. Mergers and acquisitions that involve Chinese firms or investors will be subject to more wide-ranging national security reviews and exposed to more seemingly random political interventions. Restrictions on the sale of technologies that have potential national security applications will expand. Anti-corruption, tax, public procurement, and other rules will be also rolled in to bolster national defenses. Chinese investors, tourists, and students will be told to avoid the United States, and their American counterparts in China will face increased scrutiny and restrictions. U.S. products and firms will be subject to social media–fueled boycotts in China, and “Made in China” could become a tainted tag. Trust, the basis of all business relationships, will erode.

The ability of the Chinese or American business communities to shape the relationship is limited. When NAFTA was at risk, Canadian and Mexican business leaders engaged their counterparts in the United States to lobby for the continuation of free trade. Presently, the American and European business communities are jointly rallying to preserve free trade between the United States and the EU. The Chinese business community does not have such friendships: foreign businesses and investors have complained for years about an unequal playing field and strategic threats when operating in China. And, presidents Trump and Xi have placed a premium on national identity and on securing the support of their respective business communities. In short, China-U.S. relations are likely to get worse before they get better.

Brexit: Where is the UK headed?

Prime Minister Theresa May came to power following the 2016 Brexit referendum saying that she was battle-tested and the right person to deliver the will of the people. Alas, her performance has crushed any confidence in her ability to lead the nation and see it through its most important policy challenge. There are many complaints about her performance, but May’s predicament reflects that of the nation: hubris about having cake and eating it too has succumbed to the reality that the UK has no leverage in the divorce.

Because it has taken so long for the UK to come to terms with the EU, negotiators have essentially agreed to a transition deal that preserves the status quo until at least the end of 2020, with an uncertain relationship expected to emerge thereafter. In effect, May has arrived at a very soft Brexit. But Dublin and Brussels are also insisting on a border-free Ireland, and the presumed weakening of the relationship between Northern Ireland and Great Britain—plus the lack of a clean break with the EU—has thrown the British parliament into political paralysis.

Accordingly, Brexit remains one of the most tangible global risks heading into 2019. With the clock ticking down to March 29, three broad paths stand before the nation: crash-out, deferral, or cancellation. The May government has said it will not try to pass its unpopular deal until mid-January, and by then Brexit will only be 10 weeks away.

As policymakers argue, companies will start panicking about their supply chains because customs and border inspection wait times are expected to surge from minutes to days, health providers will fret about acute shortages of medical supplies, and travelers will be warned against plans to venture abroad. Facing a growing prospect of economic paralysis, parliament may succumb to May’s transition deal. Brussels has a reputation for last-minute fixes, and to avoid the worst effects of a crash-out, the EU, too, will offer last minute deferrals to avoid near-term disruption.

Many Brits remain hopeful that Brexit will be cancelle—most likely through a second referendum. In a significant ruling, the European Court of Justice in December said that such a move would be permissible. In a November survey of UK voters, 54 percent of respondents said they would vote to remain in the EU.

Calling off Brexit would eliminate tremendous economic uncertainty and adjustment costs for business, investors, and workers, but it would not solve the UK’s profound political problem: the 46 percent who still want Brexit would be deeply dismayed and angry at their politicians for failing to pull it off. The Conservative Party is already pulling itself apart over Brexit, and the abandonment of its signature policy could lead to the election of a hard-left Labour government, which would likely bring its own style of political chaos and economic destruction.

By ridding itself of a pesky UK, Brussels could focus on the EU’s pressing existential problems: slow growth, border security, common defense, fiscal integration, and rising nationalism.

While the economic risks of Brexit for the EU are more diffuse, there are significant political risks. The specter of Brexit gave rise to a surprising degree of consensus among the remaining 27 EU member states, in part because of the bloc’s vexation with Britain’s ambivalence to EU integration over the past four decades. By ridding itself of a pesky UK, Brussels could focus on the EU’s pressing existential problems: slow growth, border security, common defense, fiscal integration, and rising nationalism. A drawn-out Brexit or outright cancellation will extend the diversion risks for Brussels and which could ultimately contribute to crashing the EU. In any event, should the UK remain in the EU, its political clout will be greatly diminished.

The bigger picture is that although the British have asserted that they are not European, the people and their political leaders have no clear vision of what they want their country to be in the 21st century. The UK faced down a referendum on Scottish succession in 2014, and Northern Ireland’s ties with Great Britain look more tenuous than ever. Given the political mess, Brits may take a cue from France and hit the streets in violent protest (egged on, of course, by Moscow). The country’s reputation for maintaining a stiff upper lip and muddling through will be put to the test in 2019.

Innovation: Technology becomes politicized

Breathtaking technological advances will again be a dominant theme in 2019. For example, the rollout of 5G wireless networks will allow for further development of the internet of things, mobile commerce, and autonomous vehicles. 5G also will create profound economic leapfrogging opportunities, especially for emerging and frontier markets. But just as important, the technology narrative is bifurcating: businesses and investors are focused on opportunity and transformation while citizens and governments are increasingly focused on risks and information control.

Technology companies set out to develop so fast that they will disrupt others, including governments, before they get disrupted, but governments are poised to put the brakes on tech companies in 2019. Technoskepticism in Europe will intensify on several fronts in the coming year, particularly over enforcing the General Data Protection Regulation and antitrust measures as well as curtailing profit shifting and tax base erosion. Technoskeptic urges in the United States are clearly on the rise, though the divided government will slow developments.

Perhaps the most significant issue in 2019 will be how debates on technology are confounded by geopolitics.

Perhaps the most significant issue in 2019 will be how debates on technology are confounded by geopolitics. Countering Russian interference in elections and political movements and restricting Chinese technological and intellectual property encroachment will continue to gain in importance. While tech companies will be promoting the borderless cloud, governments will be trying to draw national boundaries around critical data flows and technologies that are deemed essential to national security. Finally, cybercrime will evolve into cyberwar and businesses will find that attacks on their data systems and operations will not only be an economic threat, but also an everyday tool used by state and non-state actors for geopolitical advantage.

The rest of the world: Idiosyncratic or systemic risks?

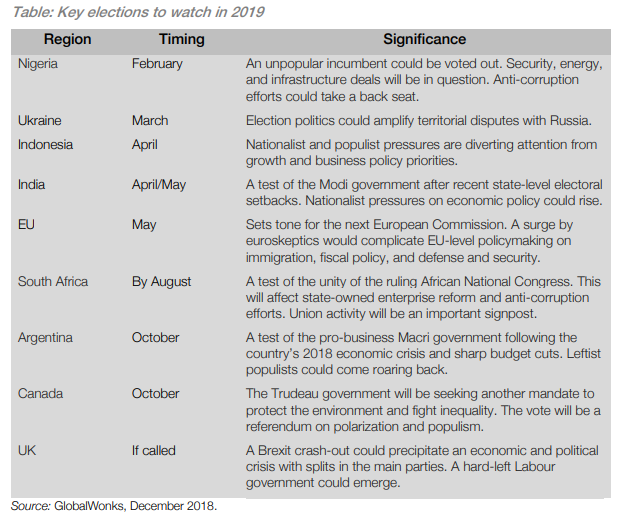

Many of the countries to watch in 2018 are on the list again in 2019. These include Mexico, Brazil, the United States, France, North Korea, Saudi Arabia, and Iran. There will be a number of important elections to watch in the coming year as well. While many of the issues at hand are domestic, they also have significant cross-border implications. Moreover, in-country developments are likely to be impacted by the global issues outlined above.

An overarching issue to watch in the coming months is whether country-specific or “idiosyncratic” risks materialize and align to have systemic effects that depress global business and investor sentiment and economic growth.

Although political risks did not appreciably impact global market sentiment in 2018, as the year comes to a close, the global risk narrative has rapidly evolved and become more sensitized to individual developments. An overarching issue to watch in the coming months is whether country-specific or “idiosyncratic” risks materialize and align to have systemic effects that depress global business and investor sentiment and economic growth. Conversely, could blaring headlines lead to an overreaction in the markets?

Read the full article here.

_____________________

DJ Peterson is a member of the Pacific Council and the president of Longview Global Advisors.

This article was originally published by Longview Global Advisors.

The views and opinions expressed here are those of the author and do not necessarily reflect the official policy or position of the Pacific Council.